As we outlined in our introduction to the vintage, Bordeaux 2017 eludes generalisation. Striking arbitrarily, the late April frost resulted in a heterogenous Bordeaux vintage in terms of both volumes and quality.

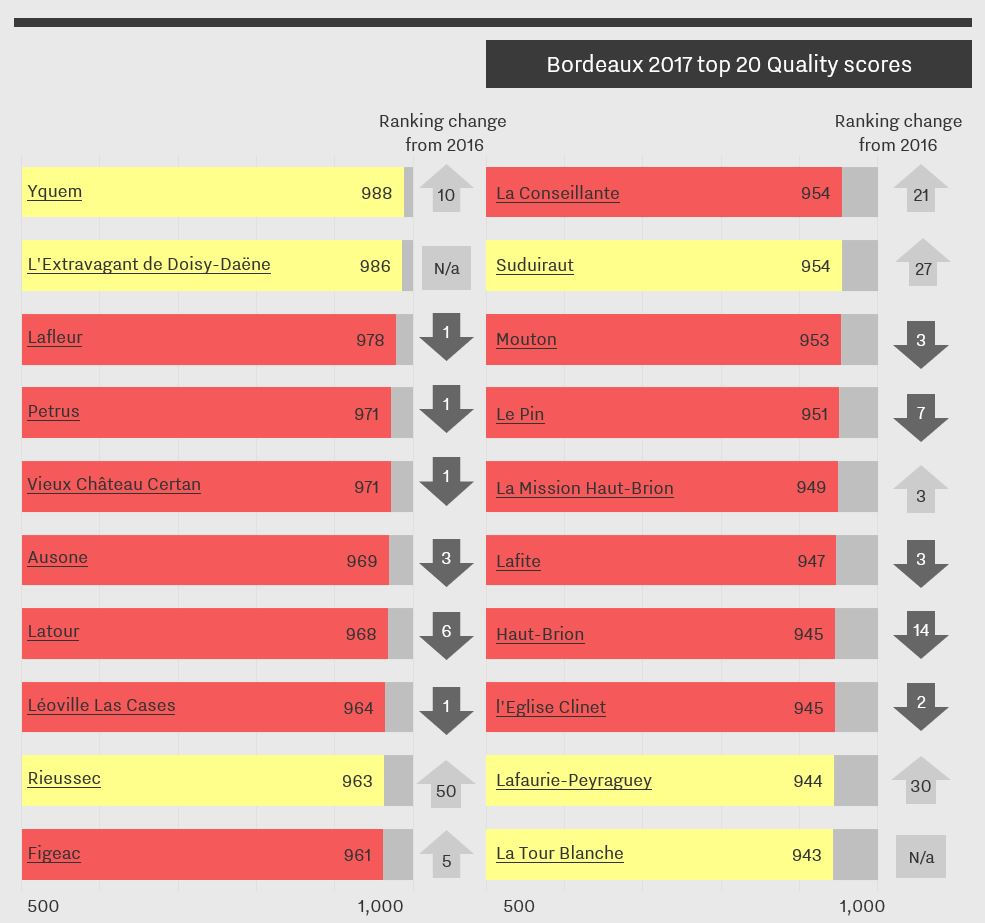

Ahead of the official release of Wine Lister’s latest Bordeaux Market Study tomorrow (don’t forget to subscribe to secure full access, via the Analysis page)*, here we give you a preview of the top 20 Quality scores for Bordeaux 2017. Wine Lister’s Quality scores for Bordeaux 2017 are based on the recently-released scores for four of our five partner critics** – Jancis Robinson, Bettane+Desseauve, and Vinous’ Antonio Galloni and Neal Martin – as well as a small weighting for longevity:

The frequent flashes of yellow in the chart above are testament to the kindness of the 2017 vintage to Bordeaux’s sweet whites, with Yquem and L’Extravagant de Doisy-Daëne achieving first and second places (scoring 988 and 986 respectively). Other sweet wines, Rieussec, Suduiraut, and Lafaurie-Peyraguey make some of the largest gains on their 2016 positions. Sauternes & Barsac stand out as the only appellations whose combined 2017 Quality score is above that of the 2016 (up 21 points).

When it comes to reds, the right bank fares best, and is home to seven of the vintage’s top 10 wines, five of them from Pomerol. Lafleur is the top-scoring red (in third place overall) with a Quality score of 978, followed by Petrus and Vieux Château Certan on 971 apiece. Pomerol’s La Conseillante makes the largest strides of any red wine in the top 20, up 21 places since 2016.

Overall, Pomerol is the highest-scoring appellation of the vintage, with an average Quality score of 959 (nonetheless down 25 points from 2016).

The left bank has fared less well with two of the five left bank appellations seeing score decreases of c.10% (Margaux and Saint-Estèphe, achieving 850 and 829 respectively). Despite dropping six places – from the top spot last year – Latour wins the left bank crown, followed by consistent overperformer Léoville Las Cases.

Other wines featuring in the top 20 Bordeaux 2017 Quality scores are: Ausone, Figeac, Mouton, Le Pin, La Mission Haut-Brion, Lafite, Haut-Brion, l’Eglise Clinet, and La Tour Blanche. You can view Quality scores for wines outside the top 20 here.

*Now published: for more analysis of the 2017 vintage, subscribe to read our Bordeaux Study.

**Jeannie Cho Lee was unfortunately unable to travel to Bordeaux to taste this year.

“I can’t see it being a big campaign.” That is the view of Serena Sutcliffe, Honorary Chairman of Sotheby’s Wine, echoed by some on the Place de Bordeaux. The usually upbeat Mathieu Chadronnier, Managing Director of négociant CVBG, asserts that 2017 Bordeaux en primeur “will be a weak campaign compared to last year”.

This sentiment is also recognised in the semi-official line, from Emmanuel Cruse, Grand Maître of the Commanderie du Bontemps, Médoc, Graves, Sauternes, and Barsac. “We all know that over the weeks to come the distribution of this vintage could be slightly more difficult on the commercial side than previous ones,” he accepted, adding reasonably, “We need to recognise that each vintage has its fair price.”

The general (if not unchallenged) consensus is that prices will come down on 2016. “Of course they will,” said Chadronnier, “but not enough.” “We always wait for decreases and they’re never considered enough,” he continued, then asking, rhetorically, exasperated, “what is enough?”

What is enough indeed? Perhaps more than ever before, there is no one size fits all formula. Just as quality and style vary from château to château in 2017 (see part I of our en primeur round-up), so will pricing. Each property has its own brand trajectory, 2017 vintage quality, volume considerations, and price positioning history. This has been epitomised by the wildly different approaches of the first two major releases of the campaign, Palmer and Haut-Batailley.

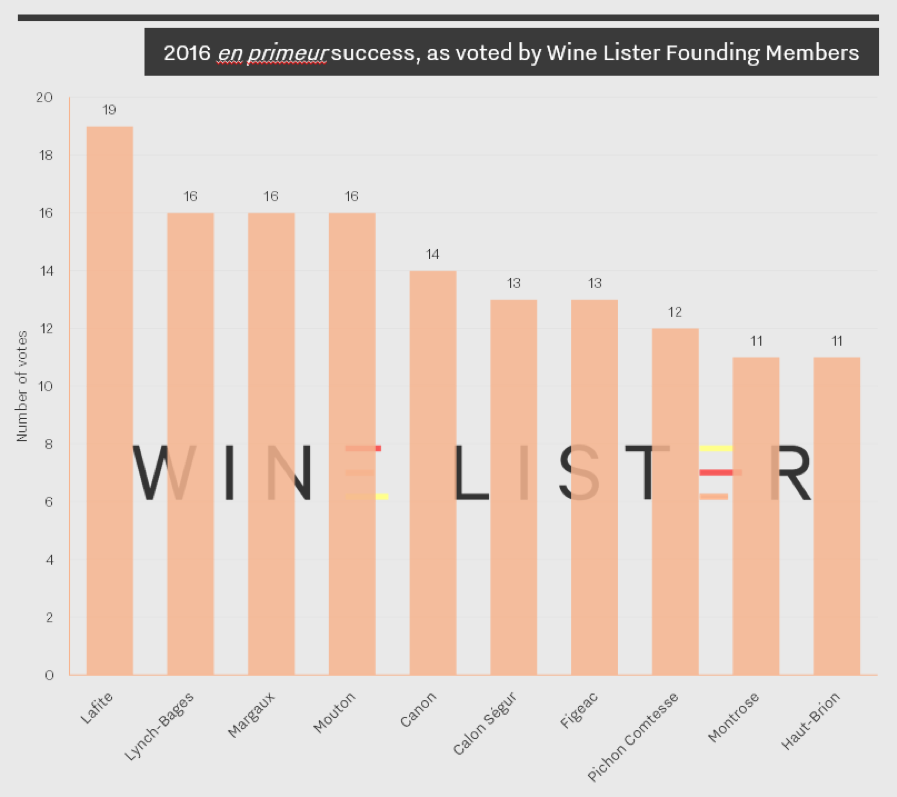

Only a small group of wines can get away with staying around 2015 prices (15-25 according to one Bordeaux courtier). Even fewer, if any, can maintain their 2016 release price. Contenders are arguably the big success stories of the 2016 en primeur campaign. According to Wine Lister’s Founding Members (c.50 key members of the international fine wine trade), first growths aside, these were Châteaux Lynch-Bages, Canon, Calon Ségur, Figeac, Pichon Comtesse, and Montrose.

However, when we put it to some of these producers that they were among a happy few potentially in a position to maintain 2016 prices, most dismissed the idea. “I could even go up and people would buy it,” mused Laurent Dufau, Managing Director of Calon Ségur. “But I won’t”, he concluded, adding “I would rather maintain the trade’s goodwill”. Nicolas Glumineau, Managing Director of Pichon Longueville Comtesse de Lalande, replied firmly, “If the question is will the price be like 2016, the response is evidently not”. He continued, “I’m really very happy with the wine we’ve made, but it’s not the 2016”.

In fact, almost every château we spoke to in Bordeaux said it would reduce the price. “It would not be right to release the 2017 at the same price as the 2016,” said Jean-Valmy Nicolas, Co-Managing Director of Château La Conseillante. “In my opinion our pricing strategy should be based on relative quality, not relative volume,” he said, referring to the impact of the frost on production volumes (down 15% on 2016).

As much as anything else, most Bordelais won’t risk the reputation of the 2016s. For most, following significant price increases for the 2016 vintage, a decrease for 2017 is manageable. This was precisely Edouard Moueix’s point (Managing Director of négociant Jean-Pierre Moueix) when he lamented, “People always compare to the year before, so even if there’s a 10-15% decrease on 2016 it’s still too high.”

For a handful of properties whose 2015s and 2016s were relative bargains, bringing the price down too much in this vintage is going to be a harder pill to swallow. Problematically for them, the market does still think in terms of increase or decrease on the previous vintage, even if this is an overly simplistic approach.

“I don’t believe for a second that prices will go down,” declared Nicolas Audebert, Managing Director of Châteaux Canon and Rauzan-Ségla, two of Bordeaux’s rising stars. Canon was voted the fifth most successful release of last year’s en primeur campaign. This is thanks to the combination of its rising popularity and its reasonable 2016 release price – it sold like hotcakes. Its 2016 price has risen by 23% since release, so arguably it is one of the very few wines that could conceive of not decreasing its price this year.

The only other château to suggest that a price decrease was by no means a given was Cos d’Estournel. Faced with the generalisation of 2017 as below the level of the last two vintages, owner, Michel Reybier, told us that “for us, compared to 2016, the 2017 vintage might even be better.”

Smoke and mirrors: Bordeaux’s Miroir d’eau (water mirror) on the only sunny day of Wine Lister’s en primeur tasting trip. Photo © Ella Lister

Farr Vintners summed up their thoughts on pricing succinctly, saying “if prices are at around the current market for [2014, 2013, 2012 and 2011], 2017 starts to look very interesting,” cautioning, “at close to current 2016 or 2015 prices the wines will not be worth buying.” Will the threat of not selling be enough to moderate producers’ pricing ambitions?

“They couldn’t care less whether they sell,” said the car hire attendant who rented me my car at Bordeaux airport. If the news has spread that far out of the wine industry, maybe it’s true. Certainly, for a gilded group of crus classés the idea of keeping back stock and selling it for more down the line is appealing. And for what they do release, they can be pretty certain their négociants will back them up and carry the stock (and the risk), even if there are few end buyers.

This was confirmed by one large négociant, who told us off the record, “We’ll buy but we won’t sell as much as we want to.” He is “worried about prices,” citing “the usual Bordeaux spiral.” He was referring to the transition period required after a string of good vintages, during which prices are not recalibrated sufficiently. “Châteaux sold the wine last year, everyone’s happy, so they won’t come down enough,” he concluded.

As for timing, we’ve already seen important releases this week, earlier than expected, with Palmer coming out a day earlier than Cos d’Estournel’s surprise release last year, in spite of the tastings taking place a week later. Nonetheless, a long campaign is expected, in part due to an inordinate number of bank holidays in May (in France and the UK). Philippe Dhalluin, Managing Director at Mouton Rothschild, seemed to predict this when he told us “it is not a speculative campaign so it should start off quite quickly.” He added, “We’d like to have an early campaign but May is complicated,” specifying, “I’d like to release before Vinexpo – it’s possible.” Anything is possible in love and en primeur.

Follow us on Twitter and on the blog for real-time coverage of the Bordeaux 2017 en primeur campaign. Check www.wine-lister.com next week for a new dedicated en primeur page where you can find out everything you need to know during the campaign.

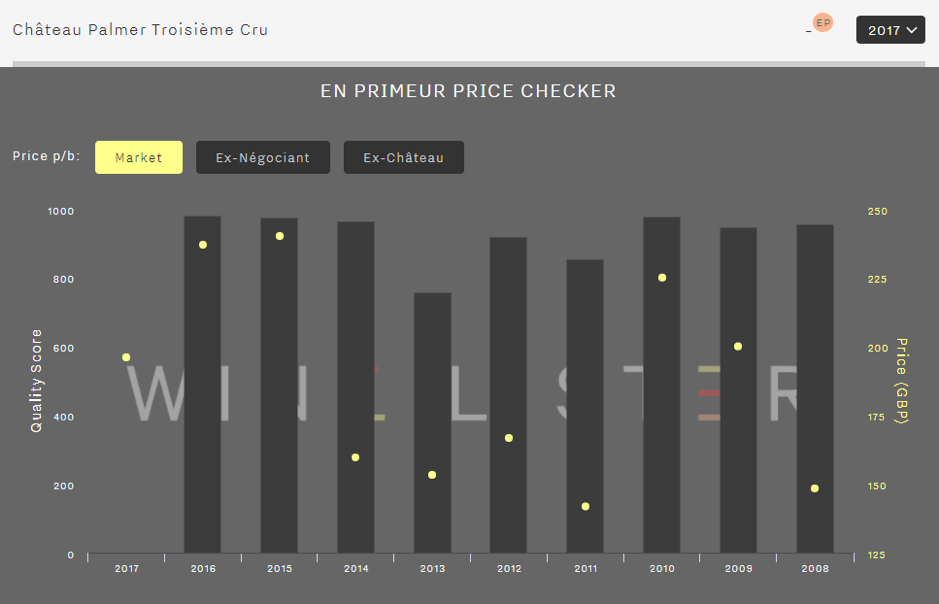

Margaux’s Château Palmer made a surprise move on Monday morning, releasing its 2017 vintage en primeur before anybody expected. At €192 ex-négociant, its price decrease of 20% on the 2016 (€240) is symbolically significant.

For several years the château has only released 50% of its Grand Vin en primeur each year, which has allowed it to develop an aggressive pricing policy, positioning itself well above other third growths and even second growths. The wine’s price had risen 14% for the 2016 vintage, giving it some margin to come down again this year. This neatly places the 2017 between the 2014 and 2015, both in terms of original release prices and current market prices:

This was a smart and strategic move by Managing Director, Thomas Duroux. When we tasted at the château in the second week of April, he shared his thoughts on the campaign, and it was clear he had considered the dynamics of 2017 Bordeaux en primeur very carefully.

Duroux was cautious about the campaign, saying “It’s going to be complicated as there are lots of discouraging factors.” He believes it’s difficult to achieve three good campaigns in a row, and that there is not a huge amount of demand from consumers. He spoke of a confusion around price and volumes, explaining that “just because there’s less wine doesn’t mean consumers are ready to pay more – they don’t care.” As it happens, the Grand Vin was spared frost damage in April 2017, while 15ha of the second wine was hit. Alter Ego was released at just a 2% discount on the 2016.

“We risk having a campaign where prices go down but not enough to be judged attractive by the consumer,” warned Duroux. It remains to be seen whether Palmer 2017’s 20% decrease is enough. With the trade unprepared, and scores not out yet for many important wine critics (including Wine Lister’s partner critics), it is now a waiting game. Négociants have bought their allocations, and for now they are holding a fair amount of stock of Palmer 2017 in Bordeaux.

Sales by UK merchants are modest for the time being. Depending on scores that will be released over the coming 10 days, Palmer might start to seem like a good deal, particularly when (not if) the discounts start to shrink over the course of the campaign. Or indeed when the discounts become premiums, as we saw this morning with the release of Haut-Batailley 2017 – read the blog post here).

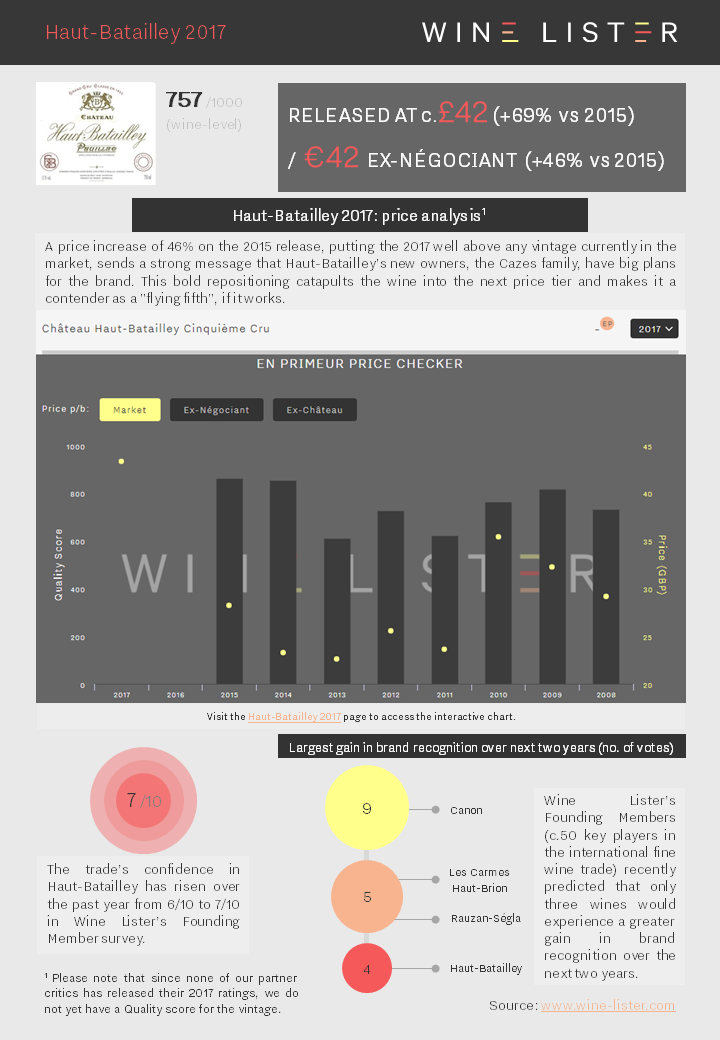

Bordeaux en primeur analysis of Haut-Batailley 2017, which has been released this morning at €42 ex-négociant, 46% up on 2015 (€28.80). It is being offered in the UK at c.£42, 69% above the 2015 release price (£25):

You can download the slide here: Wine Lister Factsheet Haut-Batailley 2017

If you hadn’t already heard about the frost in 2017, you soon will. It was the word on everyone’s lips during last week’s en primeur tastings in Bordeaux. Production volumes were down 40% across the wine region as a whole, with some properties losing their entire crop. Meanwhile others escaped entirely, making Bordeaux 2017 a vintage where both quantity and quality vary greatly from château to château.

The April frost was a “snob”, according to Will Hargrove, Head of Fine Wine at Corney & Barrow, because the very top vineyards were often spared (Petrus and Ausone for example). However, illustrious châteaux such as Cheval Blanc and Figeac might beg to differ. Nonetheless, such less lucky châteaux expended considerable resources to manage frost damage.

Véronique Sanders, Managing Director of Château Haut-Bailly, called it “the vintage of ice and fire”, referring to the dry summer months that followed. Indeed, the weather conditions resulted in many very good wines in 2017, especially suiting Cabernet Sauvignon, which as a result features in greater proportions than usual at many châteaux.

“I will not try to tell you that 2017 is at the level of ’15 or ’16, but if they are great vintages then ’17 is very good.” Those were the words of Olivier Bernard, owner of Domaine de Chevalier and President of the Union des Grands Crus de Bordeaux. “It will be a lovely wine to drink, I promise you,” he continued. The Wine Lister team is in full agreement.

Throughout our six days of tasting, in the Médoc, the Graves, and on the right bank, we were pleasantly surprised over and over again by the quality of the wines, and positively stunned by some, inter alia Les Carmes Haut-Brion, Cos d’Estournel, Figeac, La Fleur-Pétrus, Petrus, Pichon Comtesse de Lalande, Vieux Château Certan. (We can’t wait to find out what our partner critics think, and will add their scores to the website as soon as they’re released).

Part of the Wine Lister team kicking off their week of en primeur tastings at Petrus. Photo © Wine Lister Limited

Part of the Wine Lister team kicking off their week of en primeur tastings at Petrus. Photo © Wine Lister Limited

While it is not an easy vintage to generalise about, the Bordeaux 2017s tend to boast vibrancy and freshness. This allows the unique character of each wine to shine through. “I think people understand that Bordeaux is not one style,” reflects Edouard Moueix, Managing Director of négociant Jean-Pierre Moueix, declaring that 2017 is “the archetype of the expression of that diversity,” with “each terroir overexpressed almost”.

The wines have less density and concentration than the 2015s and 2016s, but nonetheless possess the structure to carry them well into the future (while in most cases also being approachable quite early). Finding a comparable vintage is tricky. Analytically speaking, both the excellent 2005 and the difficult 2013 were cited by winemakers, but upon drinking the wines they resemble neither.

At Mouton-Rothschild, Philippe Dhalluin says the wines are somewhere between 2014 (“for the energy”) and 2015 “for the softness”. On the right bank, Moueix describes the 2017 as “like a 2006 with more controlled tannins, while Hubert de Boüard, co-owner of Angélus and consultant oenologist to dozens of other properties, is reminded of 2001 and has named the vintage “l’éclatant” (radiant, or sparkling).

“It’s certainly the best vintage ending in 7 since the famous 1947,” declared Emmanuel Cruse, co-owner of Issan and Grand Maître of the Commanderie du Bontemps, Médoc, Graves, Sauternes, and Barsac. To a hall full of Bordeaux château owners and trade at the annual Ban du Millésime dinner, Cruse confirmed that the general feeling about the 2017 vintage was “What a great surprise”. But will it be enough to catalyse a successful en primeur campaign?

Part II of this en primeur round-up will look at the upcoming campaign, considering likely timing, pricing, and volumes, and including views from Bordeaux and the international wine trade. Watch this space.

Our annual Bordeaux study will be released to subscribers in early May. Follow us on Twitter, Facebook, LinkedIn, and the Wine Lister blog for real-time analysis of the 2017 Bordeaux en primeur releases.

Wine Lister uses data from our partner, Wine-Searcher, to examine wines with increasing online popularity on a monthly basis.

This month, Château Canon sees a 7% increase in search frequency for January-March 2018 from the previous period. As predicted by our Founding Members (c.50 key members of the fine wine trade), who voted Château Canon number one wine likely to gain the most brand recognition in the next two years in the 2017 Bordeaux Market study, Canon was one of the big successes of last year’s en primeur campaign. Its brand continues to go from strength to strength, with search frequency in 2017 rising 35% between January and October. It will be interesting to see whether this year’s en primeur release has the same impact on its online search frequency as the 2016 vintage.

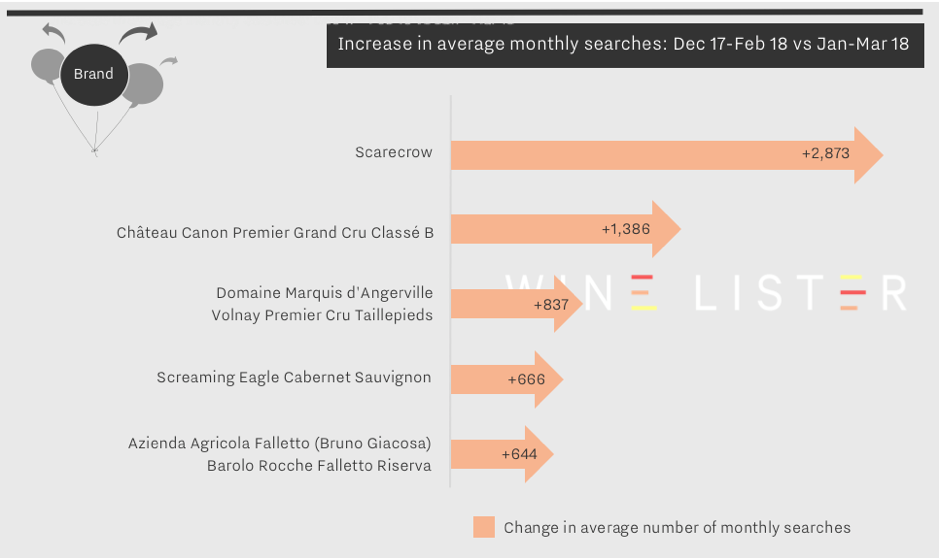

Two cult Californian wines are among the top five for latest search frequency increases.

Scarecrow saw an increased search frequency of 52% for January-March 2018 compared to the previous period thanks to its latest release in February. The 2015 vintage is as yet unscored by Wine Lister partner critics, however the estate has seen consistent Quality scores between 996-987 since 2010.

Screaming Eagle also makes the top five wines with biggest search frequency increase this month. With 17,831 average monthly searches between January and March 2018, the increase is small relative to its already vast online popularity. Indeed, Screaming Eagle remains the number one most searched for Californian wine on Wine-Searcher.

Burgundy is represented in the top search increases by Marquis d’Angerville, whose Volnay Premier Cru Taillepieds saw double its average number of monthly searches in January-March 2018 compared with the previous period. Guillaume Angerville eschews the scrum of the January Burgundy en primeur tastings in London, preferring to showcase his new vintage each March with a small tasting and lunch – the Taillepieds obviously made an impression, and achieves its highest ever Quality score (969).

Finally, searches for Azienda Agricola Falletto’s Barolo Rocche Falletto Riserva continue to rise into March following the sad passing of Piedmont legend, Bruno Giacosa. The wine saw a bittersweet rise in popularity of 14% in December 2017-February 2018, which continues at a slightly slower pace (10%).

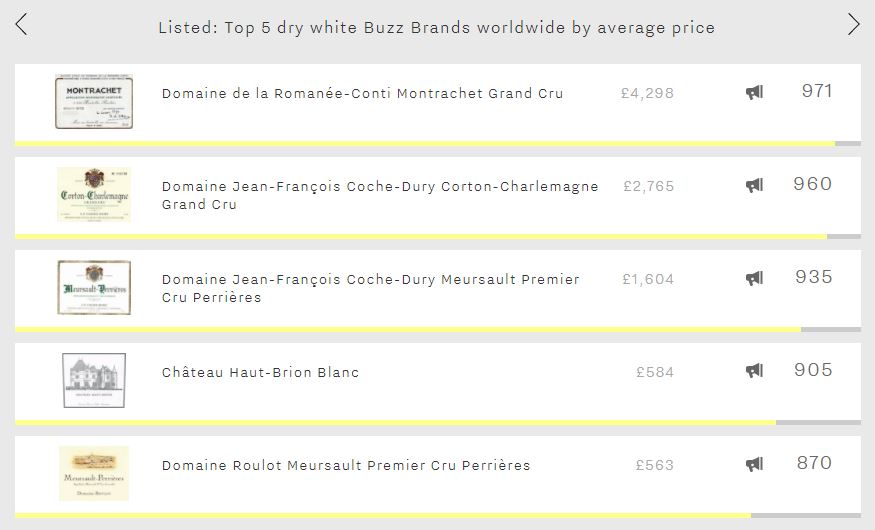

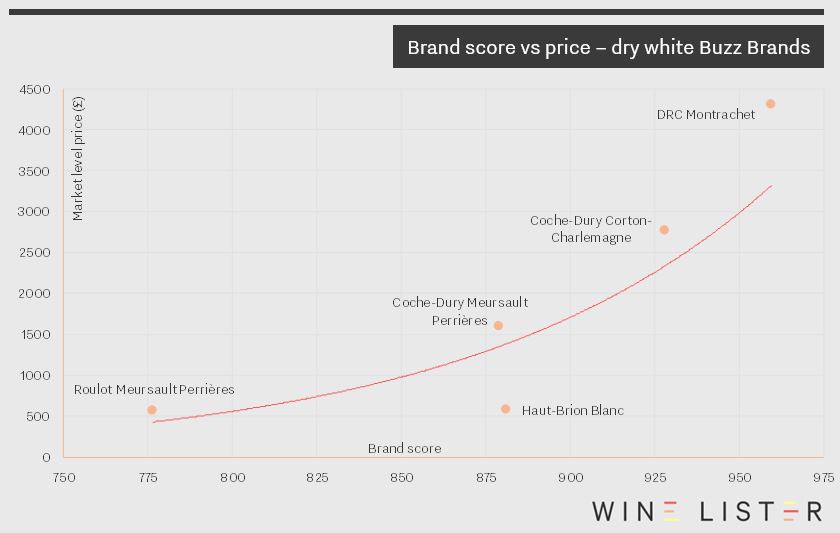

“Buzz Brands” is one of the four Wine Lister Indicators developed to help our users identify wines for different scenarios. A Buzz Brand is a wine with strong distribution in the world’s top restaurants, enjoying high levels of online search frequency or demonstrating a recent growth in popularity, and identified by the fine wine trade as trending or especially prestigious. As such, you wouldn’t expect them to come cheap, and the five most expensive dry whites definitely don’t, costing around £2,000 on average.

Perhaps unsurprisingly given the miniscule production of its top wines, Burgundy fills four of the five spots (and two of these are from Coche-Dury). DRC Montrachet is the world’s second-most expensive dry white – behind Leflaive’s Montrachet which fails to achieve Buzz Brand status. It achieves the best Quality score of this week’s top five (976), just pipping Coche-Dury’s Corton-Charlemagne to the post (971). It also enjoys the highest Brand score of the group – or any dry white for that matter (960) – the result of appearing in considerably more of the word’s top restaurants than Coche-Dury’s Corton-Charlemagne, which comes second in that criterion (26% vs 19%), and also being nearly 50% more popular than any of the rest of the five.

Whilst Coche-Dury’s Corton-Charlemagne has to settle for second place in the Quality and Brand categories, it not only manages the group’s top Economics score (991), but also the highest of any dry white on Wine Lister. This is thanks to formidable price growth. It has recorded a three-year compound annual growth rate (CAGR) of 25%, and has added 14% to its price over the last six months alone.

It is to be expected that wines from two of Burgundy’s most hallowed grand cru vineyards command the group’s highest prices, but it might come as more of a surprise that two Meursaults from the premier cru Perrières vineyard feature. With over £1,000 separating the considerably more expensive offering from Coche-Dury and Roulot’s expression, it becomes clear that Brand score is a significant driver of price at this rarefied end of the scale, particularly within Burgundy.

Proving that expensive Buzz Brands are not only to be found in Burgundy, Haut-Brion Blanc makes an appearance in the top five. Whilst it is the most liquid of the group – its top five traded vintages have traded 49% more bottles than any other wine in the five – it has experienced by far the lowest growth rates, with a three-year CAGR of 9% compared to the Burgundy quartet’s remarkable average of 22%.

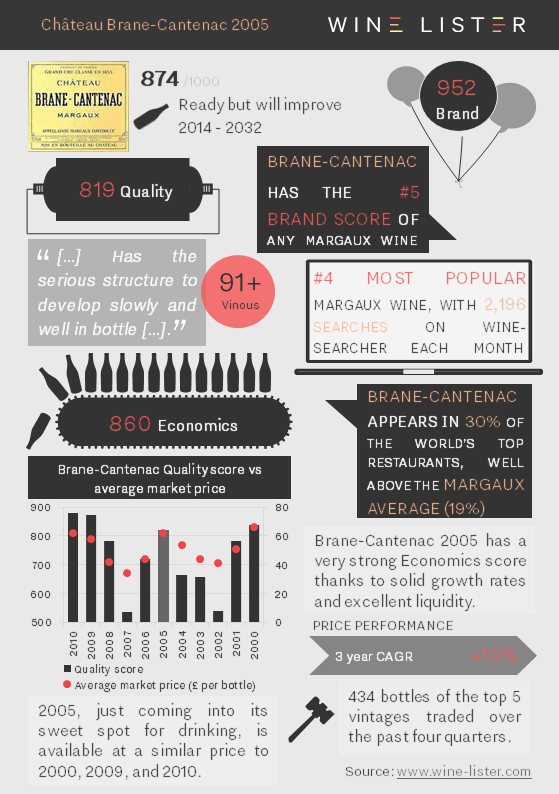

As Bordeaux en primeur 2017 tastings come to a close, we look back at Brane-Cantenac 2005, one of many highlights in our recent Founding Members’ tasting.

You can download the slide here: Wine Lister Factsheet Château Brane-Cantenac 2005

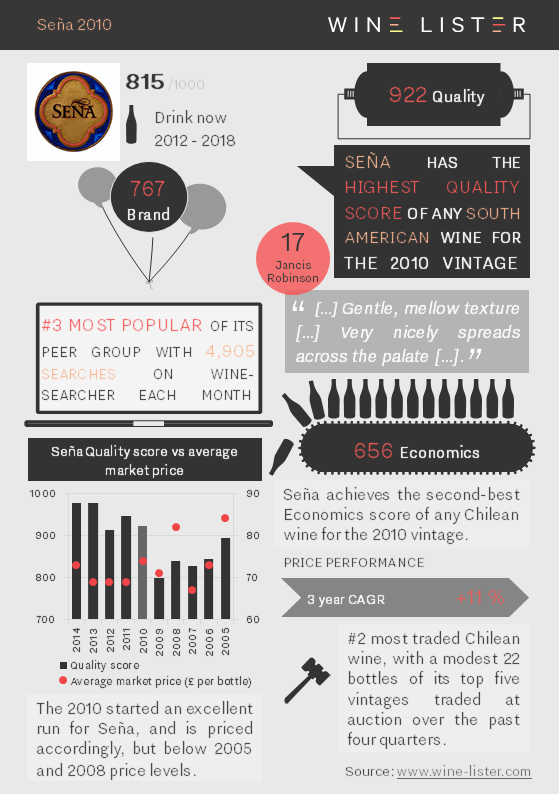

All the facts on Seña 2010, another Hidden Gem included in our Founding Member’s tasting last Tuesday.

You can download the slide here: Wine Lister Factsheet Seña 2010

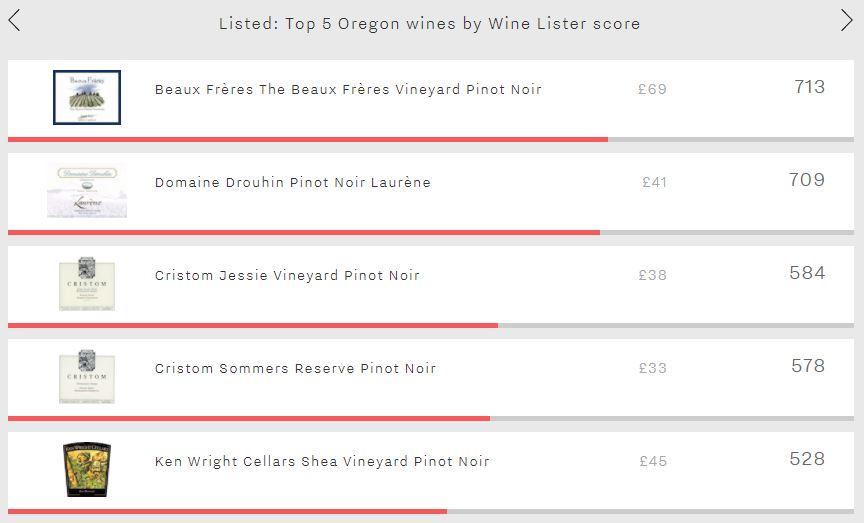

Whilst the wine world – including much of Wine Lister’s team – focuses its attention on Bordeaux for en primeur tastings, this week the blog hops over the pond to consider Oregon’s top wines. As might be expected, Oregon’s top five wines are all Pinot Noirs. Furthermore, in this relatively young fine wine region, its leading wines perform best in the Quality category (averaging 791), with their brand profiles and economic performance not yet able to keep pace (554 and 363 points respectively on average).

Whilst quality is king in Oregon, Beaux Frères Vineyard tops the table not because of its Quality score (785) – the third-best of the five – but for its stronger brand recognition. It leads Drouhin Laurène – second in the Brand category – by 113 points (715 vs 602), thanks to superior restaurant presence (9% vs 4%) and also because it receives 40% more searches on Wine-Searcher each month on average. Its Economics score of 545 is also Oregon’s strongest, but with low trading volumes and negative price growth over the past six months, this only puts it in the “average” range on Wine Lister’s 1,000 point scale, confirming that it is the area in which the region’s wines currently struggle.

Drouhin’s Laurène achieves the group’s highest Quality score (872). Produced by the Oregon offshoot of Burgundy’s Maison Joseph Drouhin, this is deemed to have the greatest ageing potential of the five, with an average drinking window of nine years, three years longer than the second-longest lived of the group – the Beaux Frères Vineyard.

Third and fourth spots are occupied by two wines from Cristom – Jessie Vineyard (584) and Sommers Reserve (578). Despite being separated by just six points at overall Wine Lister level, they display contrasting profiles. While the Jessie Vineyard achieves a superior Quality score (858 vs 770) and Brand score (490 vs 439), the Sommers Reserve nudges ahead in the Economics category (389 vs 133). This is thanks to it being the only wine of the group whose price has not dipped slightly over the past six months, instead adding 12% to its value.

The final wine of the group – Ken Wright Cellars Shea Vineyard – epitomises the profile of Oregon’s top wines, achieving its best score in the Quality category (670), a weaker Brand score (522), before experiencing its lowest score in the Economics category (220). Perhaps as Oregon continues to establish itself on the international fine wine market – and with its quality not in doubt – its leading wines will be able to build up stronger brands and economic profiles able to rival their more southerly Californian peers.