Ornellaia 2015

Ornellaia 2015 has been released at £150 per bottle. The factsheet below summarises its key points.

You can download this slide here: Wine Lister Factsheet Ornellaia 2015

Ornellaia 2015 has been released at £150 per bottle. The factsheet below summarises its key points.

You can download this slide here: Wine Lister Factsheet Ornellaia 2015

In this week’s top five, we take a break from June’s Bordeaux bias on the vinous calendar to look at the rising prices of Tuscany’s top wines.

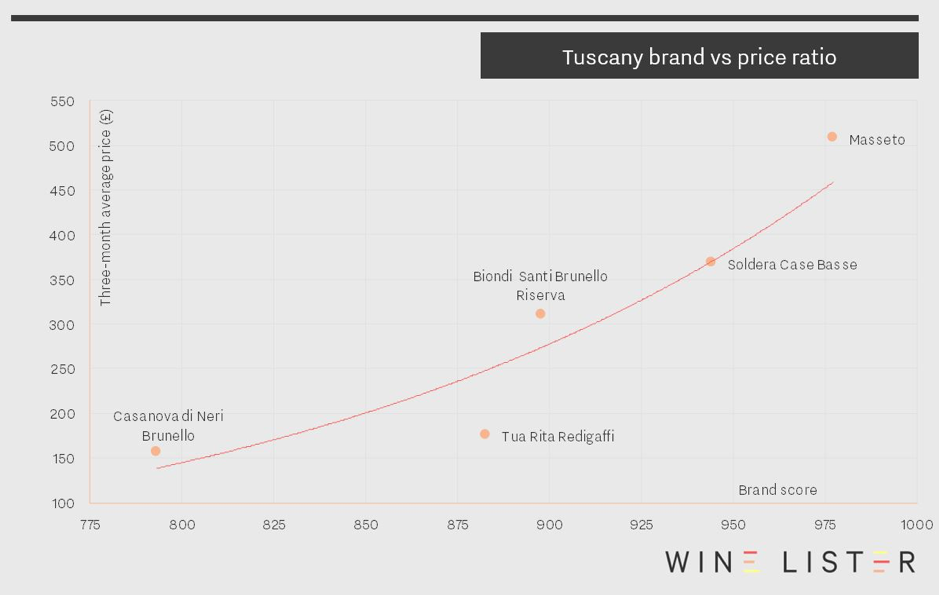

However, there’s no escaping Bordeaux with Tuscany’s most expensive wine, since Masseto is distributed through the Place de Bordeaux. With tiny quantities available to purchase via the Place each year – average annual production is 32,000 bottles – Masseto’s price of £511 per bottle makes it well over a third more expensive than the rest of this weeks’ top five, and also the second-most expensive Italian wine on Wine Lister (beaten only by Giacomo Conterno’s Barolo Monfortino Riserva).

Masseto also achieves the group’s best Brand score (977), the result of featuring in the highest number of the world’s top restaurants (24%) and being over 2.5 times more popular than any of the other four. The chart below confirms a strong relationship between Brand score and price for these wines, with Masseto’s formidable brand strength playing a key role in its high price.

At £367 per bottle, Soldera Case Basse Sangiovese takes the second spot. It achieves the highest Quality and Economics scores of the five (976 and 957 respectively). With an impressive three-year compound annual growth rate (CAGR) of 18.4% – by far the highest of the group – and having added 7.3% to its value over the past six months, Soldera Case Basse continues to cement its position as Tuscany’s second-most expensive wine, and close the gap on Masseto.

Two Brunellos feature amongst Tuscany’s most expensive wines: Biondi Santi’s Brunello Riserva (£289) and Casanova di Neri’s Brunello Cerretalto (£157). Whilst Biondi Santi Brunello Riserva’s appearance might be expected, considering its heritage, the fact that Casanova di Neri Cerretalto is amongst Tuscany’s most expensive wines might be more of a surprise, indicating that Riserva status alone does not currently guarantee higher prices than straight Brunellos.

Rounding out the five is Tuscany’s fourth-most expensive wine and the group’s second 100% merlot – Tua Rita’s Redigaffi. At an average price of £180 per bottle, it is over 2.5 times cheaper than its varietal companion in the group, Masseto.

Brands such as Sassicaia or Masseto are virtually household names. Known to most as ‘Super Tuscans’, the unofficial ‘Crus Classés’ of Tuscany’s IGT-elite have garnered a reputation for high quality and investment calibre over the last 20 years, and have a price tag to match.

Most would agree that the first Super Tuscan was Sassicaia, produced by Mario Incisa della Rocchetta, who planted Cabernet Sauvignon for his family’s own personal stock, before releasing it commercially from 1968.

The early Super Tuscan sought to by-pass the DOC system and rules banning international varieties. Labelled simply as ‘vino da tavola’, consumers were able to decide for themselves on the quality of the liquid in the bottle. Meanwhile, Sassicaia earnt its own DOCG in 2013, and has the strongest brand in Italy and one of the strongest in the world – but what of the rest?

Last month Wine Lister explored Italy’s top wines for Economics, and found that the economic profiles of Piedmont’s top wines (Barolo and Barbaresco), beat their Tuscan counterparts. So what can consumers expect from Tuscany, apart from an idyllic holiday destination?

The Tuscan crown for Brand scores still firmly sits on the heads of the big five (Sassicaia, Tignanello, Ornellaia, Masseto, and Solaia), but with a little more digging, exceptional quality can certainly be found beyond these few names. Indeed, eight of Wine Lister’s top 10 Italian Value Picks by Quality score come from the country’s central region:

Value Picks are defined as wines with the best quality-to-price ratio, with an emphasis on quality. Of the Tuscan entries, only one is a DOCG – the Chianti Classico Vigna del Sorbo Riserva 2010 from Fontodi. The others are IGT, or ‘Super Tuscan’, such as Castello dei Rampolla Sammarco 2006 and 2010, and San Giusto a Rentannano Percarlo 2010 and 2013.

On average, Super Tuscan Value Picks cost £26 per bottle, and achieve Quality scores of 864. Meanwhile Super Tuscan Buzz Brands cost six times as much for the for an average Quality score of 889.

Whether Tuscany’s classification system will be able to define a true quality hierarchy in time is not clear. In the meantime, Wine Lister’s scoring system sheds some light on where the real value of Tuscany lies.

Also featured: Isole e Olena Collezione de Marchi Cabernet Sauvignon; Domenico Clerico Barolo Ciabot Mentin; Galardi Terra di Lavoro

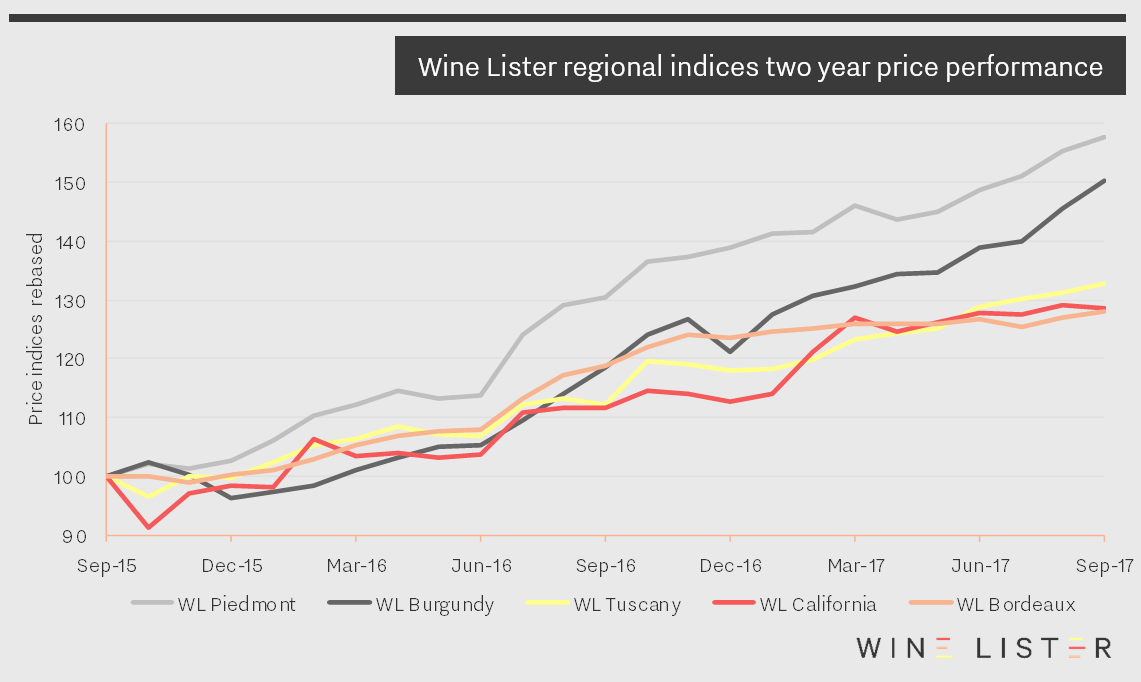

In this blog we look at the price performance of five major fine wine regions over the past two years. Wine Lister’s regional indices use price data from Wine Owners, and each comprises the top five brands in its respective region (according to the Wine Lister Brand score).

In Bordeaux, for example, the top five strongest brands (measured by looking at restaurant presence and online search frequency), are the five first growths, Haut-Brion, Lafite, Latour, Margaux, and Mouton. Posting gains of 28% over two years, and largely stagnating over the last year, the Wine Lister Bordeaux index is the worst performer of the five wine price indices shown below.

Piedmont, meanwhile, has enjoyed a remarkable couple of years. Not only has its index grown by an astonishing 58% over the period, it has also been very consistent, experiencing just three months of negative growth – November 2015, May 2016, and April 2017. Sustained high growth rates suggest a region in demand. The Wine Lister Piedmont index consists of two wines from Gaja – Barbaresco and Sperss (now labelled as a Barolo again after several years of declassification to Langhe Nebbiolo), two Barolos from Conterno – the Monfortino and the Cascina Francia, and finally Bartolo Mascarello’s Barolo.

Next comes the Burgundy index (consisting entirely of Domaine de la Romanée-Conti wines), which has grown by more than 50% over the past 24 months, but with a few more blips. It decreased in value by 4% in December 2015, only managing to recover in March 2016. In a repeat of this festive dip, the index dropped over 5% in December 2016, but recovered the losses in just one month on this occasion. It has started to close the gap on Piedmont over recent months, adding over 15% since May.

Tuscany and California* made similar gains to Bordeaux over the period – up 33% and 29% respectively. The Tuscany index has progressed fairly serenely over the past two years, thanks to its liquid Super Tuscan components. Meanwhile the prices of California’s top wines have been less consistent, enduring a fall of nearly 9% in October 2015, recovering with a dramatic 8% rise in February 2016. This year, having enjoyed strong gains during February and March, their growth rate has since cooled off, adding just 1.5% over the past six months.

*As you will know, California has suffered tragic wildfires in recent weeks. Wine Lister’s partner critic, Vinous, is donating to relevant charities the profits from all maps purchased before the end of November 2018.

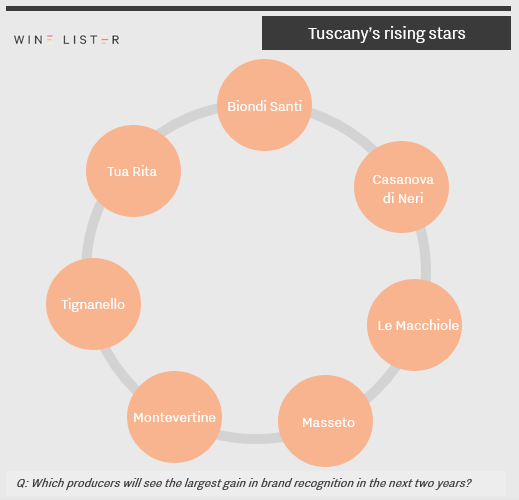

In the latest of our blogs on the findings from Wine Lister’s Tuscany Market Study – following on from a look at the region’s global standing, and the popularity of its appellations – we turn our attention to its individual wines. Here, we have carried out an in-depth survey with our Founding Members (the key fine wine trade players from across the globe, between them representing more than one third of global fine wine revenues), for insight into their confidence in Tuscany’s individual wines.

First, we asked respondents which producers are due to see the largest gain in brand recognition in the next two years. More than half those cited are producers whose flagship wines are Super Tuscans / Tuscany IGT: Tenuta Tignanello (Tignanello and Solaia), Masseto, Montevertine (Le Pergole Torte) and Tua Rita (Redigaffi).

Brunello di Montalcino DOCG is home to two contenders, Biondi Santi and Casanova di Neri, while the final producer, Le Macchiole, makes mainly Bolgheri DOC wines.

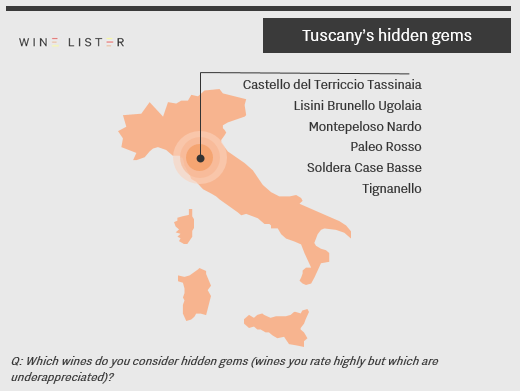

We also asked the trade which individual Tuscan wines they consider to be hidden gems: wines that they rate highly but which they perceive as underappreciated elsewhere. Two of these wines are made by rising star producers above: Tignanello, and Le Macchiole’s Paleo Rosso, suggesting that these wines may not stay underappreciated for long.

Apart from Soldera Case Basse, all of the wines cited have average prices per bottle of £75 and under, combined with strong average Quality scores that vary between 814 (Castello del Terriccio Tassinaia) and 919 (Tignanello).

To take a look at the rest of the survey’s findings – including which Tuscan wines have seen the sharpest rise in demand, which consistently sell out, and which the trade have most confidence in – please log in to Wine Lister and download the report from the Analysis page.

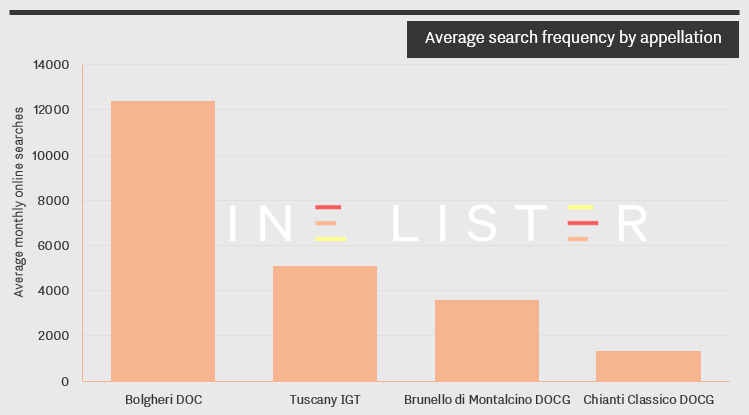

In the second blog exploring some of the findings from Wine Lister’s Tuscany Market Study – following on from our look at how the region ranks globally – we take a look at the popularity of Tuscany’s appellations. The chart below plots the average number of online searches received each month by the 50 wines in this study (based on data from Wine-Searcher), filtered by appellation.

Wines from Bolgheri DOC are by far the most popular amongst consumers, with, on average, more than twice the number of searches than their nearest competitor, Tuscany IGT. They are boosted by internationally established Super Tuscan brands such as Sassicaia and Ornellaia, which have stolen the limelight from more traditional neighbouring DOCGs such as Brunello and Chianti.

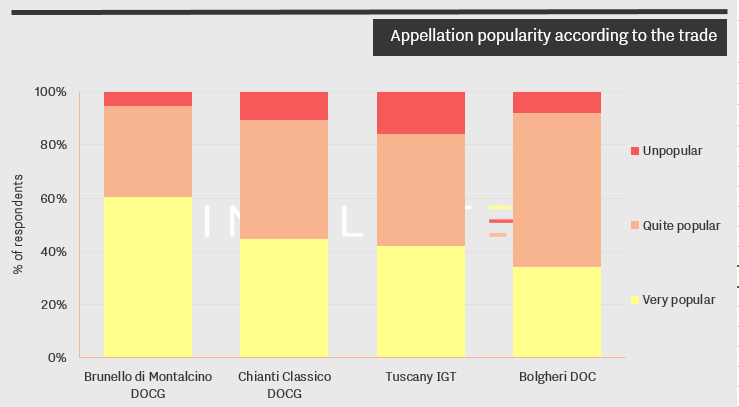

However, perception of each appellation’s popularity tells a different story. At the end of 2016, Wine Lister asked key members of the international fine wine trade about the relative popularity of Tuscan appellations amongst their clientele. Brunello di Montalcino – the third most searched for appellation – came out on top, with nearly 60% of respondents stating that it was very popular with their customers, followed by Chianti Classico.

Tuscany IGT and Bolgheri DOC trail slightly behind, emphasising that it has been the wines themselves, rather than the appellations, that have achieved fame.

In our final blog post on the Tuscany Market study we will focus in on the individual wines themselves: the trade’s view on which are the region’s consistent sellers and which are its rising stars. Wine Lister subscribers can read the full 35-page report here.

Wine Lister has produced its second in-depth regional study, this time on Tuscany – a many-faceted fine wine region that is fast-building its position on the global fine wine stage. We will be revealing some of the findings on the blog in the next few weeks, but the full 35-page report is available for subscribers on the Analysis page.

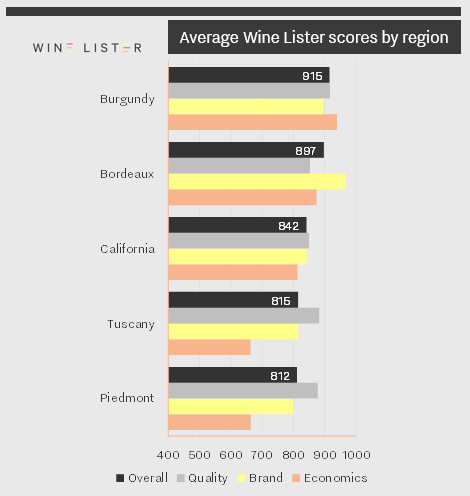

The study focuses on 50 top Tuscan wines, which we have compared below with 50 wines from Piedmont, Bordeaux, Burgundy, and California. Using the three categories that comprise an overall Wine Lister score – Quality, Brand, and Economics – we can put the region’s global positioning in context.

Although Tuscany comes fourth overall – just ahead of Piedmont – its Quality score is bettered only by Burgundy, scoring 883 points to Burgundy’s 917. Quality scores are derived from Wine Lister’s partner critics’ scores and a wine’s ageing potential, and Tuscany’s excellence in this category may be one explanation for its rising appeal.

Tuscany’s Brand score is the fourth best of the group, suggesting that after a handful of top brands such as the Super Tuscans, the rest of the top 50 do not confer the same level of prestige as wines in Bordeaux, Burgundy, or even California. Meanwhile, the region’s commercial clout is the weakest of the group, scoring one point less than Piedmont in the Economics category.

In upcoming posts, we will delve into the trade’s view on Tuscany’s foremost appellations and which are the wines to watch.

Yesterday saw the release of the latest vintage of Sassicaia, the challenging 2014 vintage. None of our partner critics has yet tasted scored the wine in bottle, but Vinous’s Antonio Galloni found the wine “promising” from barrel (read more here).

Wine Lister’s CEO, Ella Lister, recently attended a 44-vintage tasting of Sassicaia in Rome, beginning with its first commercial release, 1968. “This once-in-a-lifetime tasting proved the amazing consistency of the wines’ quality as well as their extraordinary ageing capacity”, she reported.

In the context of this release, we explore the whole gamut of vital facts about Sassicaia, a formidable wine regardless of the vintage:

You can download the slide here: wine-lister-factsheet-sassicaia-2014